by admin

Wow! 2019 is already upon us.

As 2018 soon recedes into memory, it’s time to look ahead to 2019. For small businesses, it’s crucial to consider how such items like new legislation and tax deadlines can impact your day-to-day operations and monthly schedules.

Below is a list of 2019 items we think should be on a small business owner’s radar.

Keep Up with 2019 Mileage Reimbursement Rates

At the time of writing this article, the IRS has not released the 2019 standard mileage rate. We encourage you to check the IRS Standard Mileage Rates webpage for updates.

Salespeople and anyone who has a mobile-oriented job should be aware of a Tax Cut and Jobs Act (TCJA) impact to claiming mileage as a tax deduction.

As of January 1, 2018, employees can no longer deduct mileage as unreimbursed business expense deductions. This might come as a shock to people who drive a lot for their jobs as they prepare their 2018 taxes.

However, the self-employed can still claim mileage as a business expense.

If you’re a business owner with mobile employees, you might want to consider adopting a mileage reimbursement model that can help compensate for the miles they drive.

Plan Now to Use Health Flexible Spending Arrangements

Being able to set aside pretax income to cover health care costs not paid by insurance can be a significant financial benefit for employees.

In 2019, employees (not self-employed) can contribute $2,700 through payroll deductions to health flexible spending accounts (FSAs). Deadline for 2019 enrollment was November 30, 2018.

FSAs tend to be a use it or lose it account. Money not spent by the end of the plan year can be forfeited. However, some employers may offer FSA plans to carry over $500 of unspent funds into the next year. Additionally, some FSA plans allow a two and a half month grace period to spend 2018 funds in 2019.

Meeting the January 31, 2019 Deadline for W-2s & 1099s

Yes, we’ll be facing that W-2 and 1099 deadline before you know it. In order to correct potential errors, we recommend that employers prepare and distribute these well before the January 31, 2019 deadline.

Be Aware of Social Security 2019 Maximum Changes

In 2019, the maximum amount of income subject to the 6.2 percent social security taxable ceiling increased to $132,000 from $128,400.

Take Advantage of Higher Retirement Contribution Maximums in 2019

After six years stuck at $5,500, employees can now contribute up to $6,000 in your IRA in 2019. If you’re age 50 or over you can contribute a Catch-up, limit up to $1,000.

Contributions to 401(k) increased from $18,500 to $19,000. If you’re age 50 or over, you can contribute a Catch-up, limit up to $6,000. The total contribution limit for both employee and employer increased from $55,000 to $56,000 ($62,000 for age 50 or older).

If you’re self-employed, you might want to take full advantage of contributing 20% of your self-employment earnings through a SEP-IRA. Didn’t set up a SEP-IRA in 2018? Well, it’s not too late. For those that extend their 2018 tax return date, the deadline to set up a SEP-IRA and make an initial contribution for the 2018 tax year is October 15, 2019.

Too Busy? Delegate Your Tasks

Managing a business is time-consuming. Especially when you have to keep up with all of the changes from regulations to taxes. Make time by delegating tasks to a virtual assistant firm like Business Solutions Unlimited? Call us today at (904) 429-4588 and let us start keeping up with all the small details so you want have to.

by admin

States now have the ability to apply sales tax to online purchases even if the online retailer doesn’t have a physical presence in the state.

The U.S. Supreme Court case of South Dakota v. Wayfair changes a previous court decision which established a physical retail presence was necessary to collect sales tax.

With this 5 to 4 decision in June 2018, the U.S. Supreme Court allows states to level the playing field between online purchases and local retailers. The burden of collecting sales tax may now be shared across all retailers if a state decides to take advantage of the decision.

How Online Sales Tax Works Today

If an online retailer has a physical presence in the state, they must collect sales tax from purchases made by residents of that state.

Amazon has distribution centers in Florida and collects sales taxes from state resident purchases. Other online retailers, like Wayfair, do not have a physical state presence and are not obligated to collect sales tax.

Floridians, like residents in most states, were technically supposed to voluntarily pay sales tax for their online purchases. However, in many cases, consumers don’t.

Research from the Federal Government Accountability Office estimated that states lost between $8.5 billion and $13.4 billion in sales taxes in 2017.

Sales tax funds government functions ranging from infrastructure maintenance to public education.

Basically, state residents who made local retail purchases were carrying more of a tax burden to fund government services than residents who made online purchases even though those government services are shared by all residents.

What Changes with this Court Decision?

States now have the ability to collect sales tax from online purchases. However, it’s up to the states’ Legislature and Department of Revenue to implement the sales tax.

For local retailers with only a brick & mortar presence, they will continue to collect sales tax as before. Retailers with an online presence are currently under no obligation to collect sale tax from out of state purchases.

Once a state implements an online sales tax policy, all retailers will be obligated to collect sales tax.

Staying Current with Business Changes

The sales tax decision demonstrates that the environment that small businesses operate in can change quickly and dramatically. How do busy business owners and managers keep up? Delegate.

A virtual assistance firm like Business Solutions Unlimited could help you stay one step ahead of changes that could impact your business. Feel free to give us a call at (904) 429-4588 and let’s see how we can help your business.

by admin

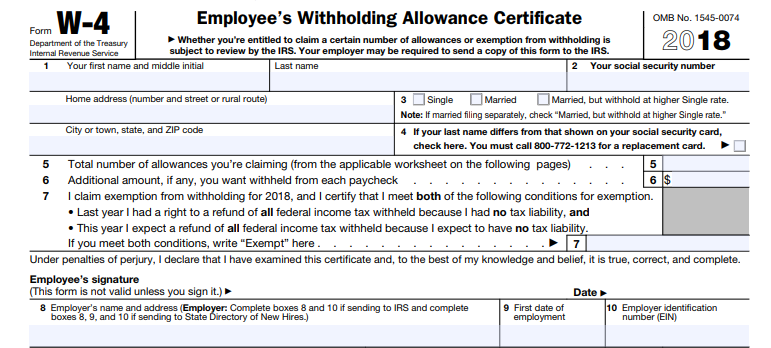

Have your employees looked at their withholding allowances on the W-4 lately?

For that matter, when was the last time you checked your withholding allowances?

If you or they typically itemize deductions and haven’t checked withholding amounts, now is the time to do so.

The Tax Cuts and Jobs Act (TCJA) went into effect this year making major changes to what we pay in taxes and the IRS encourages everyone to perform a Paycheck Checkup.

They even provided an updated online withholding calculator to help you determine the proper payroll withholding amounts for 2018.

Below, we share a link to the calculator plus tips on how to use it.

But First, Let’s Explore How the TCJA Changes Could Impact Your Withholdings

Tax law changes that affect withholding include:

- Reduced tax rates

- Elimination of personal exemptions

- Changes to itemized deductions

Additionally, the new tax law increased standard deductions to:

- $12,000 for singles

- $18,000 for heads of households

- $24,000 for married couples filing jointly

Those who claim the Child Tax Credit will see the following increases:

- $2,000 per qualifying child

- $500 for other qualifying dependents

Who Should Do a Paycheck Checkup?

If you itemize deductions, you should do a paycheck checkup. More specifically, if you:

- Are part of a two-income family

- Have two or more jobs at the same time or who only work part of the year

- Claim credits like the Child Tax Credit

- Have dependents age 17 or older

- Have high income or a complex tax return

- Have a large tax refund or tax bill for 2017

It should only take a few moments to check your withholding allowances with the calculator and make adjustments to your W-4.

How to Use the Updated Withholding Calculator

As a taxpayer, you should check at least yearly how much you’re overpaying or underpaying the government. Experts say you should withhold an amount of your paycheck that’s as close to your final annual tax bill as possible. The withholding calculator can help you determine that amount.

By the way, the calculator doesn’t ask for any identifying information like:

- Your name

- Your Social Security number

- Your address

- Any bank account numbers

Additionally, the IRS does not save or record information you enter into the calculator.

Before using the calculator:

- Gather your most recent paystubs—be sure to check that it shows the federal income tax amount you’ve withheld so far in 2018

- Get a hold of your most recent income tax return—your completed form 1040 could help you estimate your 2018 income

Once you’ve gathered the documents listed above, head over to the Withholding Calculator located on the IRS.gov website. Make sure your browser has Javascript enabled.

The IRS reminds calculator users that the calculated results are only as accurate as the information you enter. Plus, recheck your withholding amounts if your circumstances change during the year:

- Getting married

- Having a baby

Once you’ve determined your withholding amounts, download the W-4 Form and fill it out.

Need Help with Payroll, Bookkeeping or Other Business Accounting Topics?

Business Solutions Unlimited Virtual Assistants are ready to help. Give us a call at (904) 429-4588 and let’s discuss how we can help your business.

by admin

As Bookkeeping Virtual Assistants, we’re continually honing our QuickBooks skills to support our business clients.

Recently, we completed our recertification as QuickBooks Pro Advisors and became more familiar with some of the major updates to the accounting software.

Additionally, the QuickBooks course provided some helpful tips we’d like to pass on to our readers.

What’s QuickBooks Updating?

We get pretty excited when QuickBooks updates its features (consider it an accounting obsession). These four caught our attention:

- New Sales Tax Center

For businesses that collect Sales Tax, it can be a pain to keep up and update data as tax rates change. QuickBooks can now manage your Sales Tax calculations with updated information from across the nation.

Sales Tax information will be automatically updated on all new QuickBooks Online accounts & we are hoping this will be rolled out to existing accounts soon as well. All you need to do is list the state and tax agencies you need to work with.

The information QuickBooks accesses is impressive. Proper tax rates are applied to your invoices based on:

- Your address

- Your customer’s address

- Type of item sold

- Date item was sold

Additionally, QuickBooks will provide reminders to you to pay your accrued Sales Tax to the appropriate state tax agencies.

- New Projects Tab

This handy feature provides a central location to view all of your jobs along with associated transactions, notes and reports. You can view the status of your projects:

- In Progress

- Completed

- Canceled

Not only can you view, but you can add transactions directly to your project from this location.

- 24-Hour Direct Deposit for Payroll

For busy employers, this feature could be a life-saver. Previously, employers need to approve direct deposits 2-business days prior to payday.

Now, you can approve your direct deposits by 5 pm PT and still make payday the next business day.

This feature gives you:

- Greater flexibility to run payroll

- Faster time to pay employees

- Ability to hold on to your cash an extra day

- QuickBooks Capital

Small business lending moves forward with this new service from Intuit—QuickBooks Capital.

Now, small businesses can use the data compiled in their QuickBooks account to get full credit for their business performance.

The application process is embedded within QuickBooks and can be part of your daily workflow. This gives you the ability to request a loan when you need it.

Here Are Some Useful QuickBooks Tips

The following tips would be helpful for many of our business clients.

Merchant Service – ACH Bank Transfer is Free

Have you used QuickBooks to process ACH transfers? As a QuickBooks user, you can get paid quickly through ACH transfers without a fee from QuickBooks.

If you’re finding your merchant service fees adding up or taking a toll on your bottom line, this could be a valuable feature to explore.

We’d be happy to help you set up this feature.

Change Order of Your Bank Account

If you have a long list of bank accounts, it can be frustrating scrolling to find the one you want to view.

Many small businesses have accounts they need to keep an eye on more frequently than others. If that’s your case, consider reordering the list to place those important accounts at the top.

Reordering is as simple as clicking the pencil icon next to the account you want to move and dragging it where you want it. Then, click save.

Close Your Books After Each Year

It’s customary for businesses to “close the book” at the end of the year. QuickBooks automatically closes out your Income and Expense accounts and rolls up your net profit or loss into your Retained Earnings account.

However, to protect your business from changing transactions from previous accounting periods, you should consider “closing the books” with a closing date and password. This ability to set closing dates and passwords is available to both the Master and Company Administrators.

How to Get QuickBooks Assistance

It’s challenging for many small businesses to keep up with the changes and best practices of QuickBooks. That’s why our Virtual Assistants continually stay on top of the skills needed to assist our clients.

Feel free to give us a call at (904) 429-4588 to discuss how we can help you with your books.

by admin

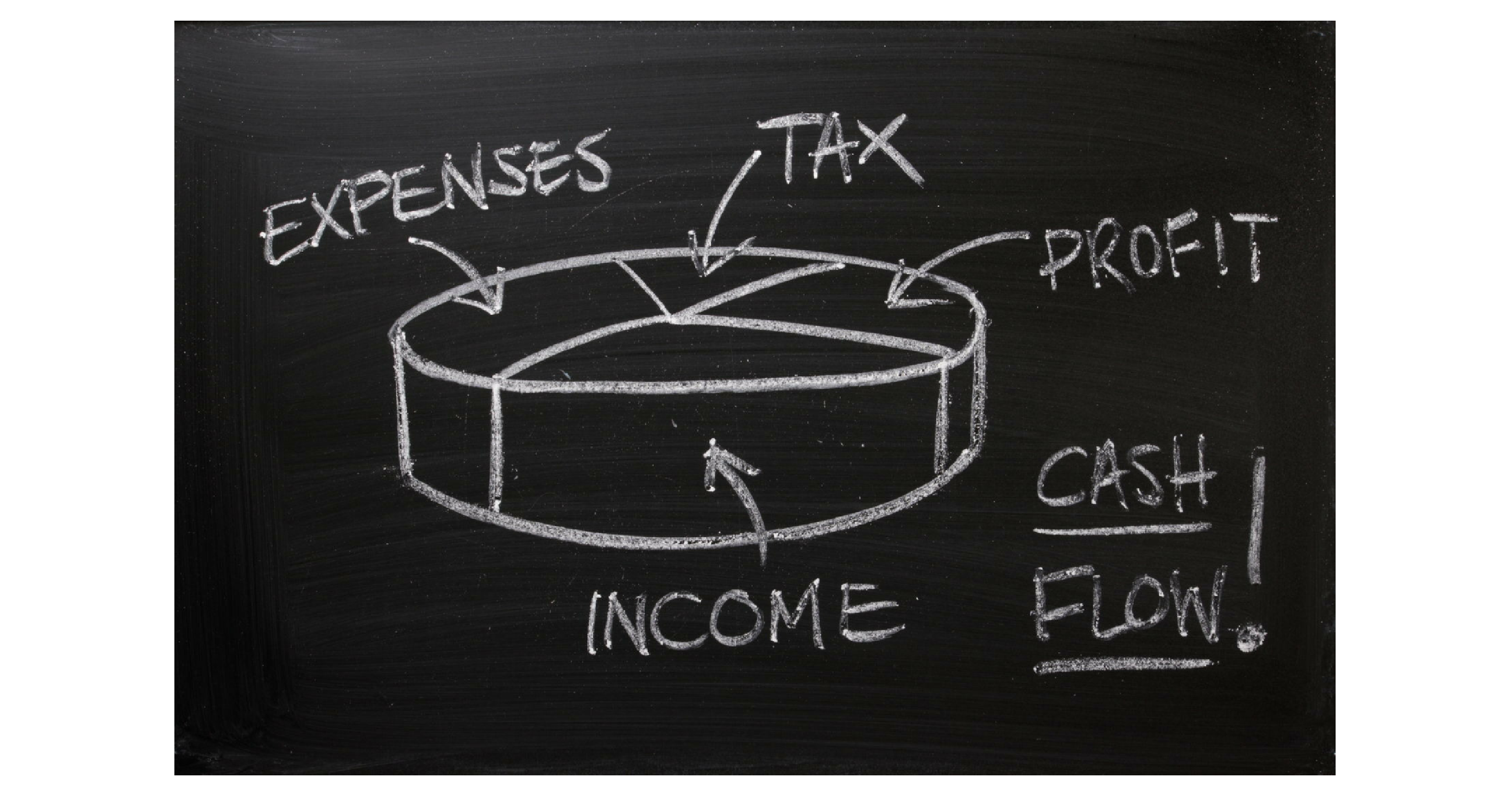

Do you know where your business dollars are?

That’s a question every small and large business manager should be able to answer quickly. Knowing where your cash flow currently sits, where it is coming from and going to, are key factors to making smart decisions about your business.

Those financial answers can be found in your financial statements.

Understanding your financial statements is relatively easy—no accounting degree required.

Over the next few minutes, we’ll show you how to read your financial statements.

Let’s Start with the Purpose of Your Financial Statement

Financial statements show the status of your business financials over a period of time—monthly, quarterly and annually. You can use the data in your statement to:

- Identify trends

- Understand your business current financial condition

- Become aware of problems requiring attention

- Make decisions based on relevant and timely information

The Three Essential Financial Statements

Typically, a business will maintain the following three financial statements:

Profit and Loss Statement (P&L): Reports on business income, expenses and profits

Balance Sheet: Provides information on the financial position of your business

Cash Flow Statement: Details how much money is coming in and going out of your business

How to Read Your Profit and Loss Statement

Your P&L will show you how revenue turns into net profit. The basic structure goes as follows:

Gross Revenue: This shows all income from sales of goods or services

Cost of Goods Sold: Cost to purchase or make the product sold

Gross Profit: Revenue minus cost of goods sold

For example: You sell a hat priced at $10. The cost of the hat is $7. The gross profit would be $3.

The next section of your P&L determines your actual Net Income (profit).

Selling, General and Administrative (SG&A) Expenses: This includes your

- Office expenses for water, pens, and coffee

- Utilities such as electricity

- Salaries or wages expenses

- Rent Expense

Operating Income: Gross Profit minus SG&A Expenses

Interest Expense: Cost of debt occurred during a period of time

Income Taxes: The total amount paid in taxes during a period of time

Net Income (Profit): Operating Income minus Interest and Income Tax Expenses

How to Read Your Balance Sheet

Look at your balance sheet as a snapshot of your business financial position. Another way to put it is the balance sheet shows the net worth of your business.

The results arrive from an accounting equation:

Assets = Liabilities + Equity

The equation must always balance because assets must be funded with either liabilities or equity.

Assets are broken down into two categories:

Current Assets

(Less Than a Year) | Long-Term Assets

(More Than a Year) |

| · Cash · Accounts Receivable · Inventory | · Office Furniture · Building/Property · Equipment and Equipment Depreciation |

Liabilities are broken down into two categories:

Current Liabilities

(Less Than a Year) | Long-Term Liabilities

(Greater than a Year) |

| Accounts Payable Including: · Sales Tax Payable · Salaries Payable · Gift Certificates | This could include a long-term loan. |

Equity is broken down into two categories:

| Retained Earnings | Capital |

An Example:

If an owner invests residual income back into the business, the amount is transferred from the income statement to the balance sheet as retained earnings. | Original funding from investor or owner into the business. |

How to Read Your Cash Flow Statement

Your cash flow statement reports on three types of activities:

Operating: Information on your business cash from net income or losses

Investing: Shows cash flow from all investment activities including purchases or sales of long-term assets

Financing: Shows cash flow from all financing activities such as a bank loan

The cash flow statement top line shows a beginning balance. Then adds or subtracts amounts based on the above financial activities. The final total amount shows the amount of cash your business has on hand.

How to Get Assistance on Your Financial Statements

As virtual assistant bookkeepers, Business Solutions Unlimited is well-versed in not only reading financial statements but maintaining them as well. If you require any assistance, we’re happy to help.

Feel free to give us a call at (904) 429-4588 and let’s see how we can help your business.

by Christie Tostevin

As our economy improves, so does the cash flow for many of St. Augustine’s small businesses.

If strong sales and profits are adding excess cash to your business checking account, don’t just sit back and enjoy the good times. Take this opportunity to get the best possible return on those funds.

That excess cash—invested right—can be used to grow your cash reserves. And those reserves can be used later to:

- Strengthen and grow your business

- Insulate your from economic downturns

- Take advantage of opportunities when they present themselves

- Paying bonuses

What is Excess Cash?

According to financial experts, excess cash is what’s left over after you’re done paying salaries, marketing, upgrading and maintaining equipment, paying rent, purchasing supplies, and paying whatever it takes to operate your business day-to-day.

Oh, make sure you understand what it will take to run your business three, six or 12 months; maybe longer depending on your business plan.

So, take a look at your spreadsheet or ask your accountant to determine if you have excess cash.

Ok, There’s Excess Cash. Now, What Do You Do With It?

Since you’re dealing with business cash, you’ll want to balance liquidity with making the highest possible return.

How much liquidity you need can be determined by understanding your cash flow cycle. That’s where understanding your business needs three, six or 12-months in the future really matters.

Once you understand your liquidity needs, you can determine an investment time frame and amount of risk you can take with your excess cash.

At this point, it’s a good practice to speak about investment options with your bank or financial advisor.

Options they will probably discuss with you could include:

- Business money market deposit accounts

- Mutual funds

- Sweep Accounts

- CDs

Investing your excess cash can help put you and your business in a position of strength. That strength can lead to greater confidence to move your business forward.

If you ever have any questions about whether you have excess cash, give us a call at (904) 429-4588. We’ll see if we can help you out or guide you in the right direction for assistance.